In this article

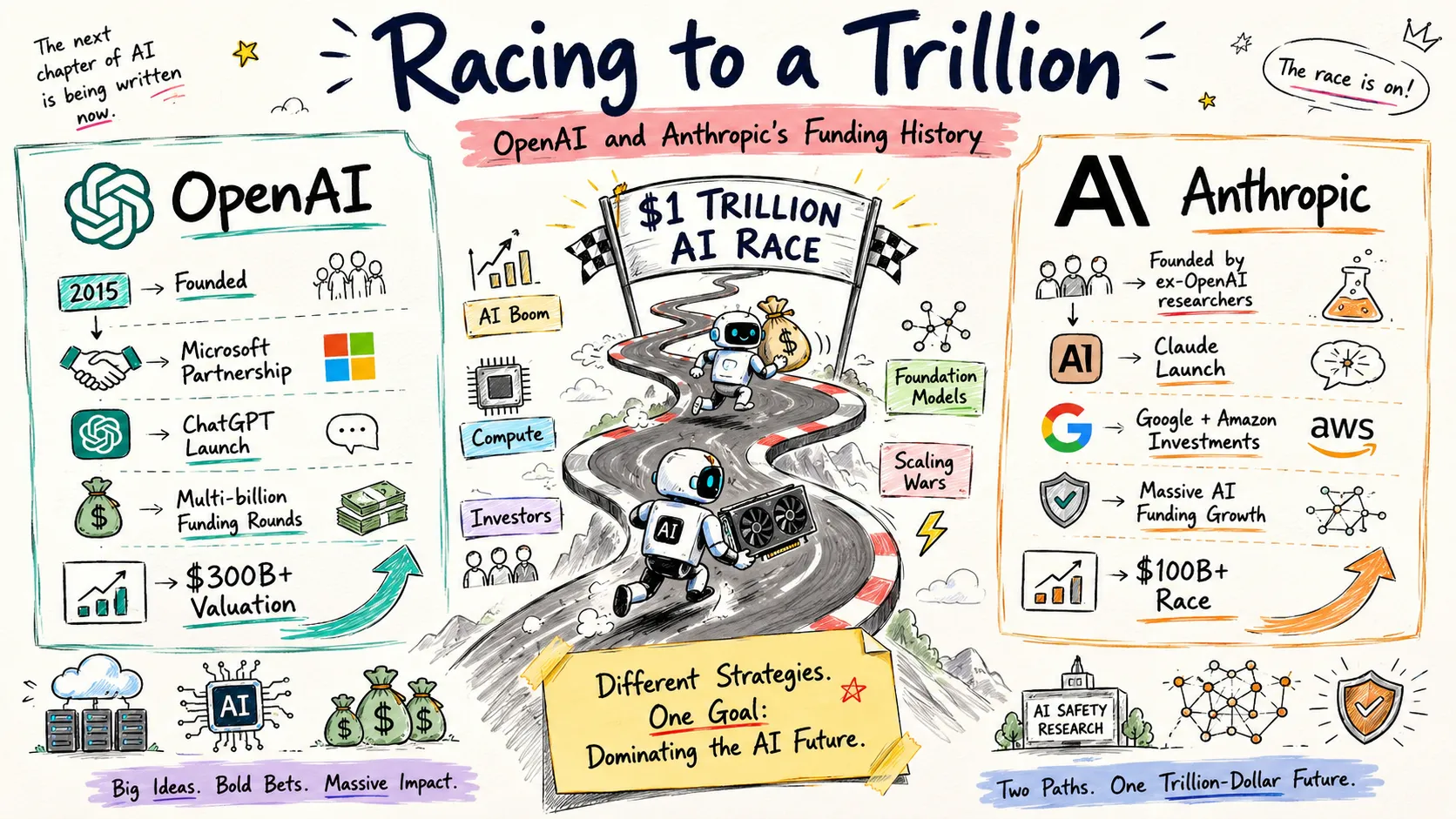

On May 28, 2026, Anthropic closed a $65 billion Series H at a $965 billion post-money valuation - briefly making it the most valuable private company in the world, surpassing OpenAI. OpenAI, for its part, closed a $122 billion round in March 2026 at $852 billion. Together, these two companies have raised roughly $300 billion between them in just a few years. The sums are so large they read more like sovereign debt than startup funding.

This post is a timeline of how both companies got here - who invested, at what valuations, what the terms looked like, and what the money is actually for.

Summary

OpenAI (as of March 2026):

- Total raised: ~$180-190 billion across all rounds

- Current valuation: $852 billion post-money

- Annualized revenue: ~$25 billion (Q1 2026); $20 billion for full-year 2025

- Key investors: Microsoft ($13B+ total), Amazon ($50B in March 2026 round), SoftBank, Nvidia, Thrive Capital, Sequoia

Anthropic (as of May 2026):

- Total raised: ~$144 billion across all rounds

- Current valuation: $965 billion post-money (Series H, May 28, 2026)

- Annualized revenue: $47 billion (May 2026); $14 billion (February 2026)

- Key investors: Amazon (up to $33B total committed), Google (up to $43B total committed; $10B immediate April 2026), GIC, Sequoia, Altimeter, Coatue, Lightspeed

The field for context:

- xAI: ~$45B raised, $230B valuation (acquired by SpaceX in February 2026)

- Mistral AI: ~$3B raised, ~$14B valuation

- Cohere: ~$1.6B raised, ~$7B valuation

OpenAI: From Nonprofit Pledge to $852 Billion

OpenAI was incorporated in December 2015 as a nonprofit research lab. The founding announcement came with $1 billion in pledged donations from a group that included Elon Musk, Sam Altman, Reid Hoffman, Peter Thiel, Amazon Web Services, and Infosys. The actual cash collected against those pledges was considerably lower - closer to $130 million. Musk personally contributed about $38 million before leaving the board in February 2018, citing a conflict of interest with Tesla’s AI work.

The nonprofit era produced real work - GPT, proximal policy optimization, OpenAI Five, various robotic manipulation demos - but it became clear by 2017 that frontier AI would cost billions per year in compute, far beyond what philanthropic donations could sustain. The team began designing a way out.

The 2019 Pivot to Capped-Profit

In 2019, OpenAI restructured into a “capped-profit” limited partnership. Investor returns were capped at 100x of invested capital (later revised downward), with any excess reverting to the nonprofit. This was unusual but coherent: it let OpenAI raise venture capital while keeping the nonprofit as the controlling entity. Microsoft saw the structure and liked it enough to move quickly.

In July 2019, Microsoft invested $1 billion, and OpenAI migrated its entire infrastructure to Azure as part of the deal. This established a pattern that would define the next seven years - large hyperscalers investing capital in exchange for strategic cloud commitments.

The ChatGPT Years (2021-2023)

A $1 billion round in January 2021 at roughly a $14 billion valuation brought in Khosla Ventures and others. Then in November 2022, ChatGPT launched and hit 100 million users in two months - the fastest user growth in consumer internet history to that point. Microsoft committed another $10 billion in January 2023 at a roughly $29 billion valuation, doubling down one month after ChatGPT’s viral moment. In April 2023, a $300 million Series E at a $28 billion valuation added Sequoia Capital, Thrive Capital, and Andreessen Horowitz.

At this point, OpenAI was a company that had just launched the most widely used consumer product in the world, and its valuation reflected it.

The Numbers Get Large (2024-2026)

October 2024: $6.6 billion at a $157 billion valuation. Investors included Microsoft, Nvidia, SoftBank, and Thrive Capital.

March 2025: $40 billion from SoftBank, Microsoft, and others at a $300 billion valuation - then the largest private fundraise in history. The Stargate initiative, a joint venture with SoftBank and Oracle to build AI data centers across the United States, was announced simultaneously.

March 31, 2026: A $122 billion round closed at an $852 billion post-money valuation, upsized from an initial $110 billion target. Amazon committed $50 billion (structured as $15 billion funded at close plus $35 billion contingent on OpenAI achieving AGI or completing an IPO), SoftBank $30 billion, Nvidia $30 billion. For the first time, OpenAI also brought in $3 billion from retail investors channeled through bank partners - a move that reads as pre-IPO positioning. Additional investors included a16z, D.E. Shaw, Fidelity, Sequoia, Thrive Capital, BlackRock, Blackstone, Temasek, and T. Rowe Price.

OpenAI’s total raised across all rounds sits around $180-190 billion.

Corporate Restructuring

OpenAI converted from a capped-profit LP to a public benefit corporation (PBC) in 2025, under pressure from investors and regulators. Microsoft’s ~27% stake shifted to the new PBC structure (valued at roughly $135 billion at the March 2026 round). The nonprofit retained a 26% stake. Critics, including several former employees, argued the conversion reduced the nonprofit’s practical control - the original structure gave the nonprofit more formal authority over what profits could be distributed and when.

Anthropic: Safety-First and Startlingly Well-Capitalized

Anthropic was founded in 2021 by seven former OpenAI employees led by Dario Amodei and Daniela Amodei. Dario had been VP of Research at OpenAI. The group’s stated reason for leaving was that safety research was being deprioritized relative to product velocity - a concern that has proven prescient as both companies have navigated questions about autonomous weapons, election influence, and AI governance. Anthropic incorporated from day one as a Delaware public benefit corporation, with a “Long-Term Benefit Trust” holding appointment power over a majority of board seats.

That governance structure is not decoration. In 2026, Anthropic declined a Department of Defense contract that would have required removing certain restrictions on autonomous weapons use - a commercially costly decision that the trust’s authority made structurally difficult to reverse even if investors wanted to push back.

The Funding Timeline

Series A (May 2021): $124 million. Lead investors: Jaan Tallinn (Skype co-founder), Dustin Moskovitz (Facebook co-founder), and Eric Schmidt. Purpose: initial research infrastructure and the team’s first model work.

Series B (April 2022): $580 million. About 86% of this round - $500 million - came from Alameda Research, the trading firm affiliated with Sam Bankman-Fried. This is the awkward entry in Anthropic’s timeline: SBF’s funds turned out to be FTX customer deposits, not Alameda’s own capital. He was sentenced to 25 years in prison. The FTX bankruptcy estate eventually sold the Anthropic stake at auction to pay creditors. Anthropic received and spent the capital before the scandal broke; the legal fallout was FTX’s problem, not Anthropic’s.

Series C (May 2023): $450 million led by Spark Capital. Separately, Google invested $300 million as part of a broader cloud relationship - the first of what would become dual hyperscaler commitments with both Amazon and Google.

Series D (late 2023 - January 2024): Amazon announced up to $4 billion in September 2023, completing $8 billion total in exchange for a minority equity stake and an agreement to make AWS the preferred cloud provider for training and inference. Qualcomm and Salesforce Ventures also participated.

Series E (March 2025): $3.5 billion at a $61.5 billion valuation. Led by Lightspeed Venture Partners, with co-investors including Bessemer, Cisco Investments, Fidelity, General Catalyst, Jane Street, and Menlo Ventures.

Series F (September 2025): $13 billion at a $183 billion post-money valuation. Led by ICONIQ, Fidelity, and Lightspeed.

Series G (February 2026): $30 billion at a $380 billion post-money valuation. Led by GIC (Singapore’s sovereign wealth fund) and Coatue, with co-investors including D.E. Shaw, Dragoneer, Founders Fund, BlackRock, Fidelity, JPMorgan Chase, Morgan Stanley, and Sequoia.

Amazon expansion (April 2026): Amazon announced an additional commitment of up to $25 billion (with $5 billion immediate), on top of its earlier $8 billion investment. Total Amazon commitment to Anthropic: up to $33 billion, making it the single largest investor by committed capital.

Google expansion (April 2026): Google announced a commitment of up to $40 billion in Anthropic, with $10 billion funded immediately. This dwarfed its earlier ~$2-3 billion across prior rounds and cemented the dual-hyperscaler arrangement as genuinely bilateral at scale, not just nominal.

Series H (May 28, 2026): $65 billion at a $965 billion post-money valuation - the largest private AI funding round in history. Led by Altimeter Capital, Dragoneer, Greenoaks, and Sequoia. Institutional investors included BlackRock, Brookfield, D.E. Shaw, DST Global, and Fidelity. Hardware manufacturers Samsung, SK Hynix, and Micron also participated as strategic investors - a compute supply chain play rather than a pure financial bet. The $65 billion figure includes $15 billion in previously committed hyperscaler tranches. Annualized revenue at close: $47 billion.

Side-by-Side Funding Comparison

| Round | OpenAI | Anthropic |

|---|---|---|

| Founding / Seed | $1B pledged (2015, ~$130M collected) | - |

| Series A | $1B, Microsoft (Jul 2019), $20B valuation | $124M (May 2021) |

| Series B / 2021 round | $1B (Jan 2021), $14B valuation | $580M (Apr 2022) |

| 2023 rounds | $10B (Microsoft) + $300M Series E, ~$29B valuation | $450M Series C + $300M (Google), ~$4.1B valuation |

| Late 2023 / 2024 | $6.6B (Oct 2024), $157B valuation | $8B (Amazon, to Jan 2024) |

| 2025 | $40B (Mar 2025), $300B valuation | $3.5B Series E (Mar), $13B Series F (Sep), $183B valuation |

| Early 2026 | $122B (Mar 2026), $852B valuation | $30B Series G (Feb 2026), $380B valuation |

| Mid 2026 | - | $65B Series H (May 2026), $965B valuation |

| Total raised | ~$180-190B | ~$144B |

The Rest of the Field

For context on how unusual these numbers are, consider xAI - Elon Musk’s AI company - which raised roughly $45 billion and hit a $230 billion standalone valuation in January 2026 after a $20 billion Series E. In February 2026, SpaceX acquired xAI in an all-stock deal valuing xAI at $250 billion. That acquisition would be the defining story of almost any other period in tech investing. Here it barely registers as third place.

Mistral, the French open-weights lab, raised a €1.7 billion (~$1.9 billion) Series C in September 2025, led by ASML, at about a $14 billion valuation. That’s a strong outcome for a company less than three years old. Cohere raised about $1.6 billion total at a roughly $7 billion valuation.

The scale gap between the frontier labs and everyone else isn’t just about ambition or market positioning. A single frontier training run for a model like GPT-5 or Claude 4 costs somewhere between $50 million and $500 million depending on run size and compute prices. The next generation is projected to exceed $1 billion per run. Companies that can’t access capital at OpenAI and Anthropic scale are necessarily constrained to smaller models, more efficient training approaches, or niche markets where their size is actually an advantage.

What the Money Is Actually Paying For

The naive assumption is that AI companies burn billions on engineering salaries. The reality is that nearly all the capital goes to compute. Training a frontier model is a one-time capital expenditure, but a large one. Inference at scale - serving hundreds of millions of API calls and end users - requires ongoing GPU capacity that grows with usage.

OpenAI scaled from about 200 megawatts of compute capacity in 2023 to nearly 2 gigawatts by 2025. The Stargate joint venture, announced alongside the $40 billion March 2025 round, committed $500 billion over four years to build AI data centers across the United States in partnership with SoftBank, Oracle, and the US government. That isn’t a software company raising growth capital. It’s a compute infrastructure buildout organized around two AI model families.

Anthropic’s approach differs in one key way: rather than building its own infrastructure, it signed long-term cloud compute agreements with both Amazon and Google. Neither investment was purely financial - both came bundled with guaranteed GPU capacity at contractually agreed rates. Amazon’s total commitment reached up to $33 billion; Google’s reached up to $43 billion after a major April 2026 expansion. Anthropic gets predictable compute access across two hyperscaler platforms. Amazon and Google each get a leading AI model on their cloud, API revenue, and equity that appreciates if Anthropic’s growth continues.

The Series H inclusion of Samsung, SK Hynix, and Micron as strategic investors adds another layer to this compute story. Memory bandwidth is increasingly the bottleneck in large model inference, and having the major memory manufacturers as investors creates alignment on the supply chain that’s hard to replicate through ordinary purchasing agreements.

Corporate Structure and Who Controls the Mission

One of the less-discussed differences between the two companies is governance - specifically what happens when commercial pressure and the stated safety mission diverge.

OpenAI spent its first four years as a pure nonprofit, restructured into a capped-profit LP in 2019, and converted to a public benefit corporation in 2025. At each step, the controlling entity’s authority over commercial decisions shifted. The original capped-profit structure gave the nonprofit explicit control: it was the general partner and could, in theory, block distributions. The 2025 PBC conversion retained the nonprofit as a significant stakeholder with a 26% equity position, but the formal architecture of control is different. Some former employees argued publicly that the conversion weakened the safety mandate by reducing the nonprofit’s veto authority.

Anthropic’s structure has been stable since founding. The Long-Term Benefit Trust appoints a majority of the board and holds authority to override decisions that conflict with the safety mission. This isn’t hypothetical protection. In 2026, Anthropic turned down a Department of Defense contract that would have required removing restrictions on autonomous weapons use. Commercially, this was a meaningful sacrifice. Structurally, the trust’s authority made it difficult for any investor to push back effectively. Whether you view this as principled or impractical probably depends on how you weigh near-term revenue against the precedents being set for how AI systems get deployed in high-stakes contexts.

Revenue vs Valuation: What the Multiples Actually Mean

At $852 billion valuation and roughly $25 billion in annualized revenue, OpenAI trades at about 34x revenue. At $965 billion and $47 billion in annualized revenue, Anthropic sits at about 20x. Traditional software companies that trade at 10-15x forward revenue are considered richly valued. Both of these numbers are well above that.

The counterargument to “these multiples are insane” is the growth rate. Anthropic’s annualized revenue went from $14 billion (February 2026) to $47 billion (May 2026) - roughly 3x in three months. At that rate, the $965 billion valuation reflects where revenue might be in six months, not where it is today. Claude Code, Anthropic’s CLI coding agent, was generating over $2.5 billion in annualized revenue by May 2026, representing more than half of enterprise spending on Anthropic - a meaningful signal that developer tools are the real growth driver, not consumer chat.

OpenAI went from $6 billion for full-year 2024 to $20 billion for full-year 2025 to roughly $25 billion annualized in early 2026. The growth rate is high, but somewhat slower than Anthropic’s recent trajectory.

The risk in both cases is the same: gross margins in AI APIs are substantially lower than in traditional software. Training costs, inference costs, and GPU depreciation are real and large. The path to profitability depends on inference costs falling faster than API pricing falls due to competition from open-weight models and smaller labs. That’s not guaranteed, and it’s the thread that, if pulled, unravels a lot of the valuation math.

Key Investors and What They Got

Microsoft invested over $13 billion in OpenAI across multiple tranches between 2019 and 2023. In return: a roughly 27% equity stake (worth ~$135 billion at the March 2026 valuation), OpenAI as an exclusive Azure customer generating substantial cloud revenue, and Copilot integration across Microsoft’s product stack. The relationship has become complicated - OpenAI restructured the revenue-sharing cap in April 2026, reducing Microsoft’s share of future profits, and both companies have begun hedging with alternative partnerships.

Amazon committed $8 billion to Anthropic in 2023-2024 (Series D), making AWS the preferred cloud provider. In April 2026, Amazon announced an additional commitment of up to $25 billion, bringing its total potential investment to $33 billion - the largest single committed position in Anthropic by any investor. AWS hosts a significant portion of Anthropic’s training workloads and distributes Claude via Amazon Bedrock.

Google invested around $2-3 billion in Anthropic across earlier rounds (2023-2024) and distributes Claude via Google Cloud’s Vertex AI platform. In April 2026, Google committed up to $40 billion more (with $10 billion immediate), bringing its total potential commitment to roughly $43 billion. The dual-hyperscaler arrangement - Amazon and Google both as large investors and distribution partners - is unusual in the industry and gives Anthropic more negotiating leverage than if it had committed exclusively to one cloud.

SoftBank invested in OpenAI across the $40 billion March 2025 round and was among the lead investors in the March 2026 $122 billion round. Masayoshi Son’s AI infrastructure ambitions align closely with OpenAI’s capital requirements.

Sequoia Capital invested in both OpenAI (Series E, April 2023) and Anthropic (Series C and later rounds), which is an unusual position for a venture firm to be in. It reflects Sequoia’s view that there may be room for more than one frontier AI winner, or at least that the downside of missing both is worse than the awkwardness of being on both cap tables.

Conclusion

Anthropic was founded five years ago by seven people who left OpenAI over research priorities. It is now worth more than most Fortune 50 companies. OpenAI, a former nonprofit, is approaching valuations comparable to the largest tech companies ever built. Whether that holds depends on revenue growth, margin improvements, and competitive position as open-weight models improve - all open questions. What isn’t in question is that the capital, the revenue, and the infrastructure being built with the money are real. For developers building on these platforms, the funding dynamics are practical: they determine which model families keep getting investment and which APIs stay reliable long-term.