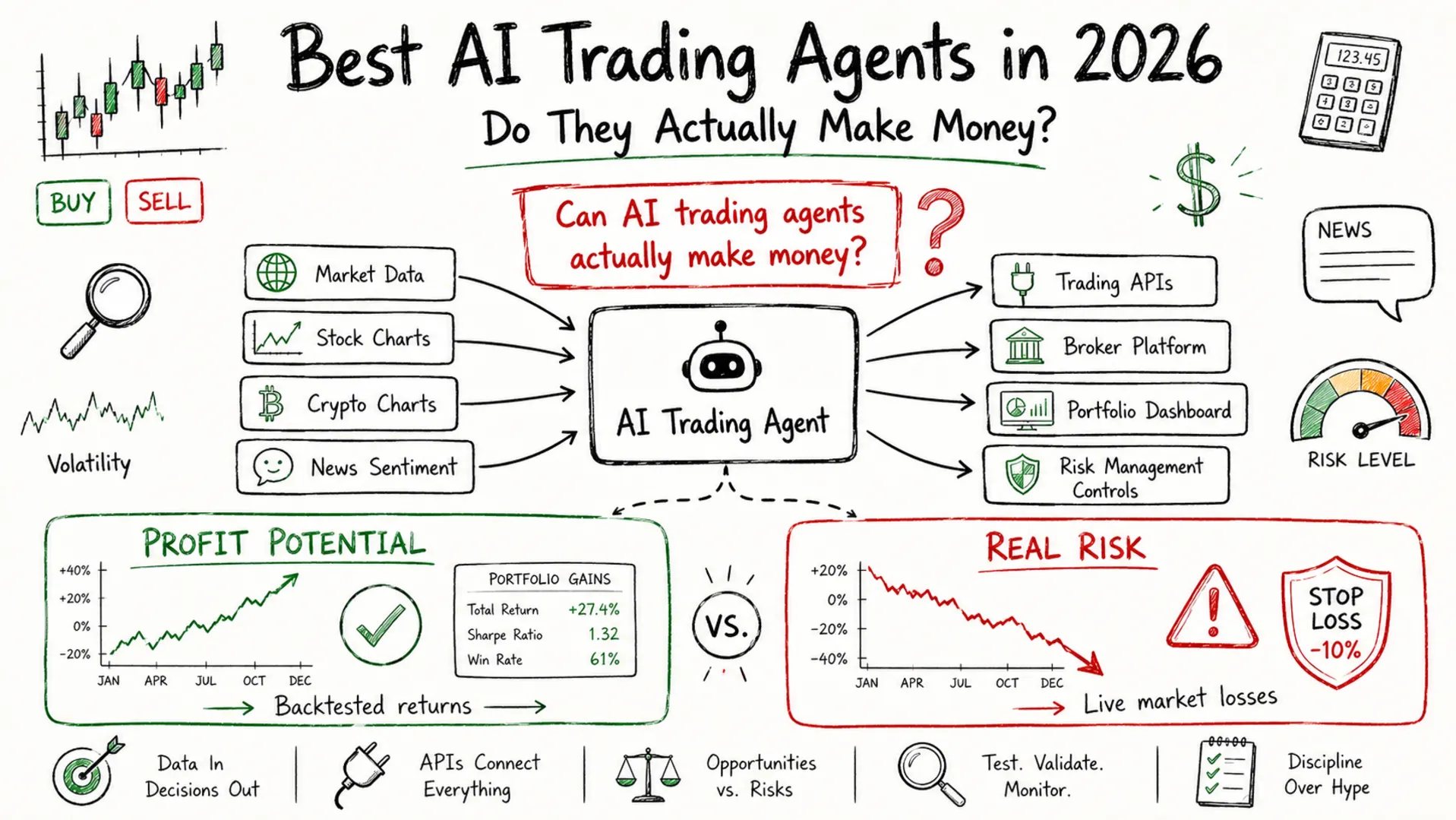

Best AI Trading Agents in 2026: Do They Actually Make Money?

The AI agent space has quietly invaded finance. Where quant funds once needed years to build trading systems, open-source frameworks now let a developer spin up a multi-agent LLM setup that reads earnings reports, monitors news sentiment, and generates buy/sell signals - all in an afternoon. The interesting question is not whether these systems are technically impressive. They are. The real question is whether they can actually make money.

This post covers the best open-source AI trading agent frameworks available in 2026, starting with a complete setup walkthrough for TradingAgents, followed by the other frameworks worth knowing, and ending with an honest look at what realistic performance expectations should be.

Summary

Top Open-Source AI Trading Agent Frameworks:

- TradingAgents - Multi-agent LLM framework simulating a full trading firm, 80k+ GitHub stars - GitHub

- AiHedgeFund - 59k+ star framework deploying 14 legendary investor personas (Buffett, Munger, Burry, and others) plus analytical agents to debate stock picks - GitHub

- FinRL / FinRL-Trading - Deep reinforcement learning framework (15k+ stars) with a production-ready deployment layer (FinRL-Trading) that adds live Alpaca broker integration - GitHub

- FinRobot - LLM agent platform for automated equity research report generation - GitHub

Can they make money? In backtesting, yes - sometimes impressively. In live trading, the gap between simulated and real returns is large. Transaction costs, slippage, and market regime changes all eat into performance. One documented TradingAgents run achieved roughly 7% returns over 30 days vs the S&P 500’s 4.5% for the same window - but with 22% drawdowns and no guarantee of repeatability. These are research tools and learning platforms first, not passive income generators.

How AI Trading Agents Actually Work

The key shift from traditional algorithmic trading is using LLMs as reasoning engines rather than hardcoded rule systems. Classic algo trading is explicit: if RSI drops below 30, buy. AI trading agents replace that fixed logic with natural language reasoning. An LLM reads earnings transcripts, news articles, social media, and price data, then reasons about what that information means for a stock’s near-term direction.

The most sophisticated frameworks go further by deploying multiple agents with distinct roles, mirroring how a real trading firm is structured. A fundamental analyst agent digs into financials. A sentiment agent reads news. A technical analyst looks at chart patterns. A risk manager sets position limits. Each agent produces a report, and a trader agent synthesizes those reports into a final decision. The structured debate between agents helps surface conflicting signals before a trade is placed.

This multi-agent architecture is less prone to single-point bias than a single LLM deciding in isolation. But it comes with real costs: more API calls, more latency, and higher per-signal expenses. A full analysis run for one ticker can cost $0.30-$0.50 in LLM credits at GPT-5 rates. Running this daily across a portfolio of 20 stocks is not cheap.

TradingAgents: Complete Setup Walkthrough

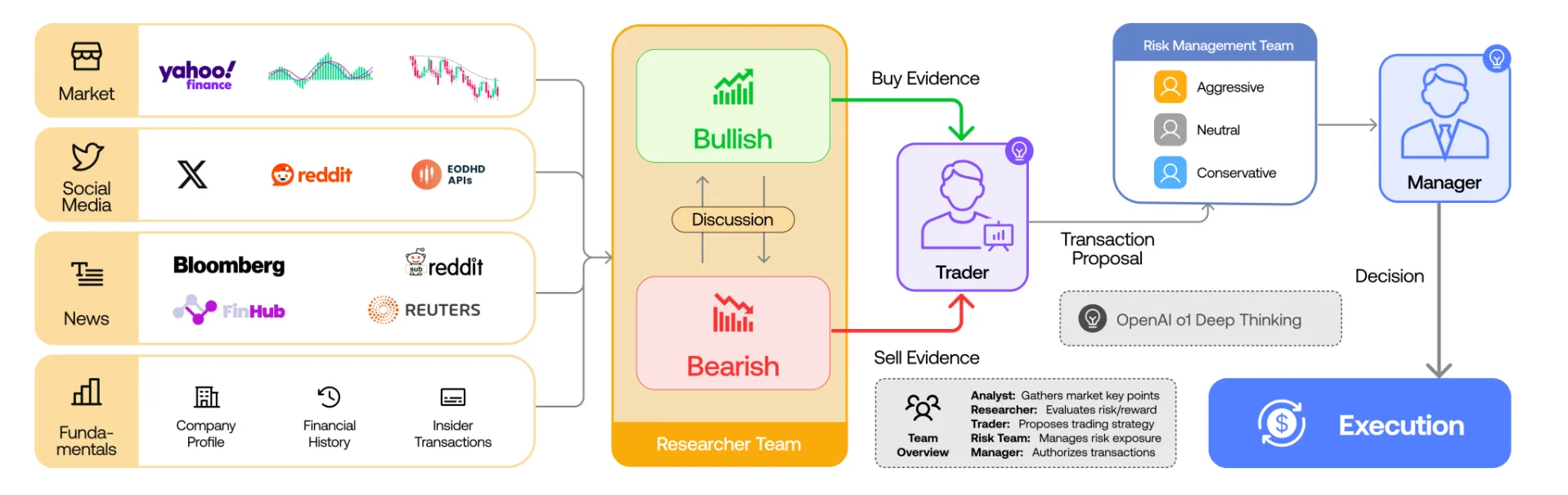

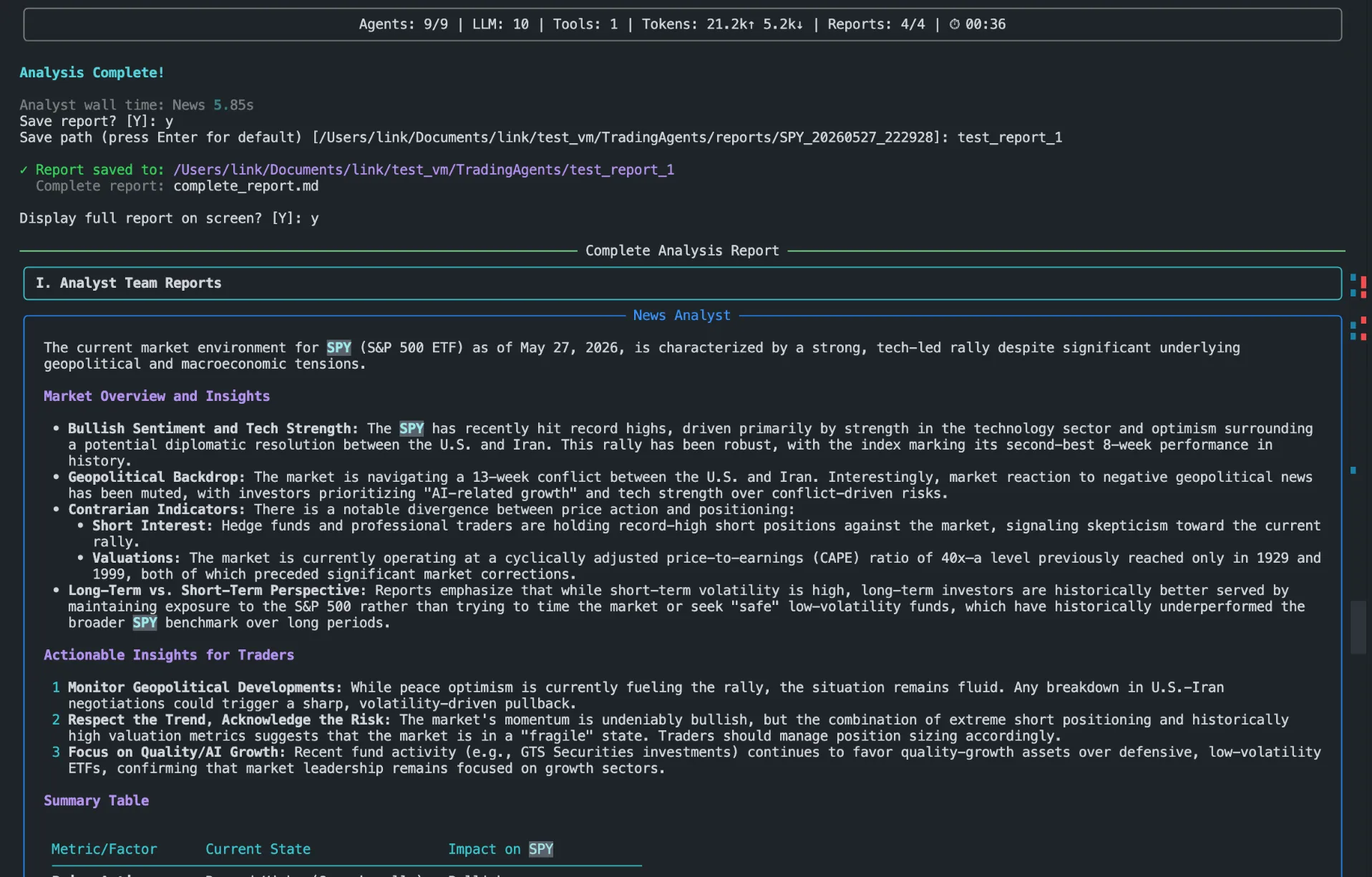

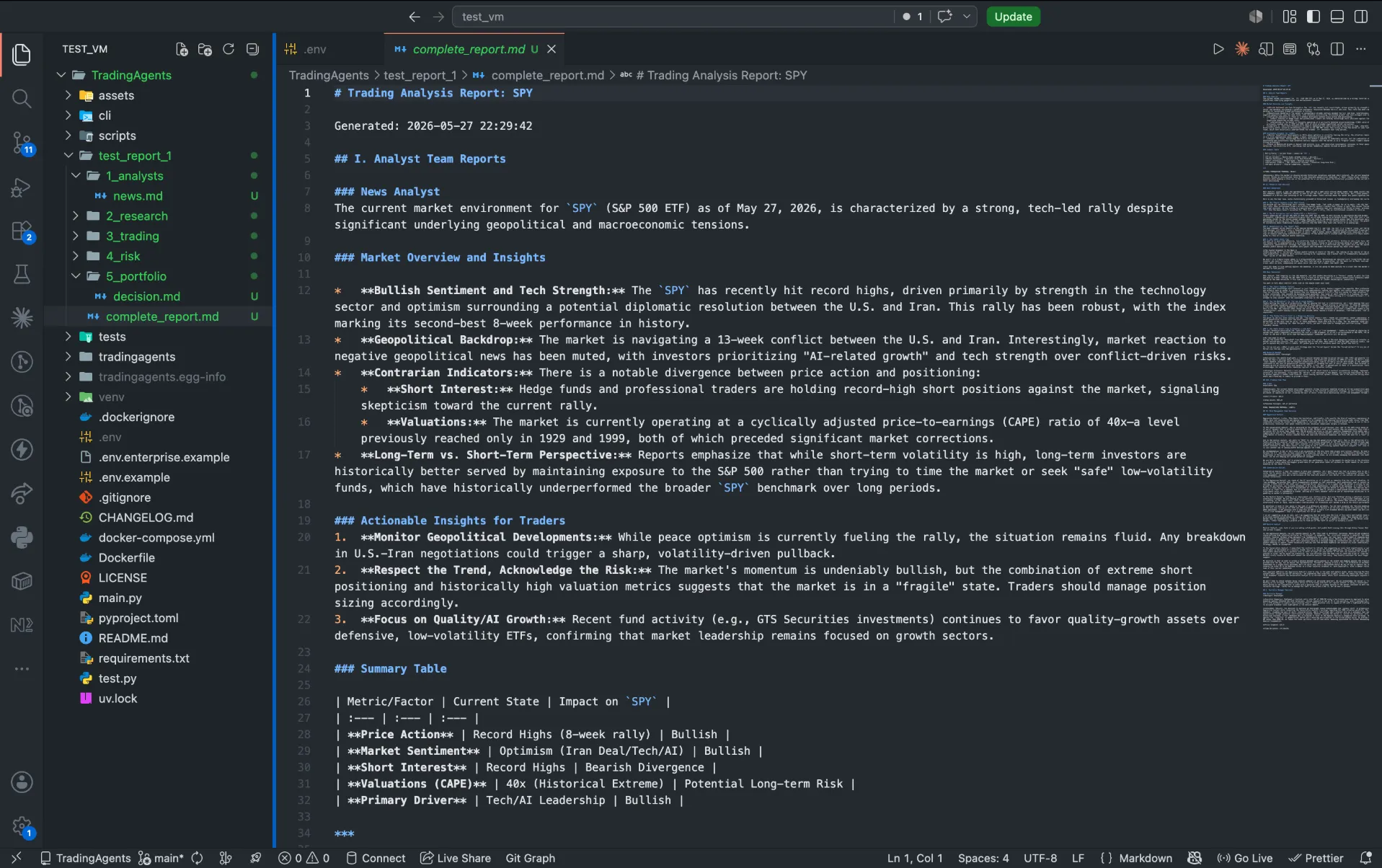

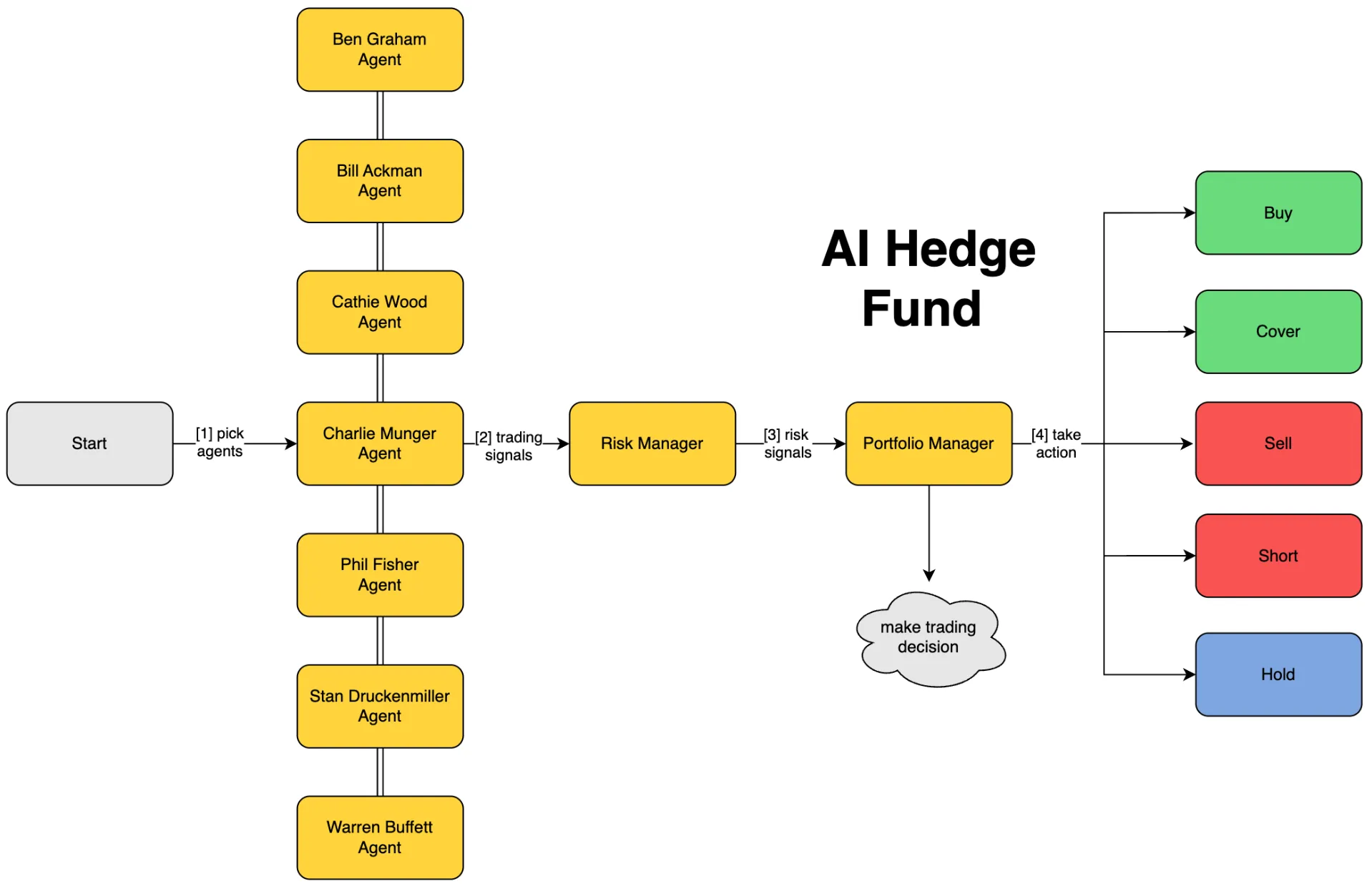

TradingAgents by TauricResearch is the most-starred open-source AI trading framework on GitHub with over 80,000 stars and 15,500 forks. It models a real trading firm by deploying LLM-powered specialist agents who collaborate through structured debate to analyze markets and generate trading decisions.

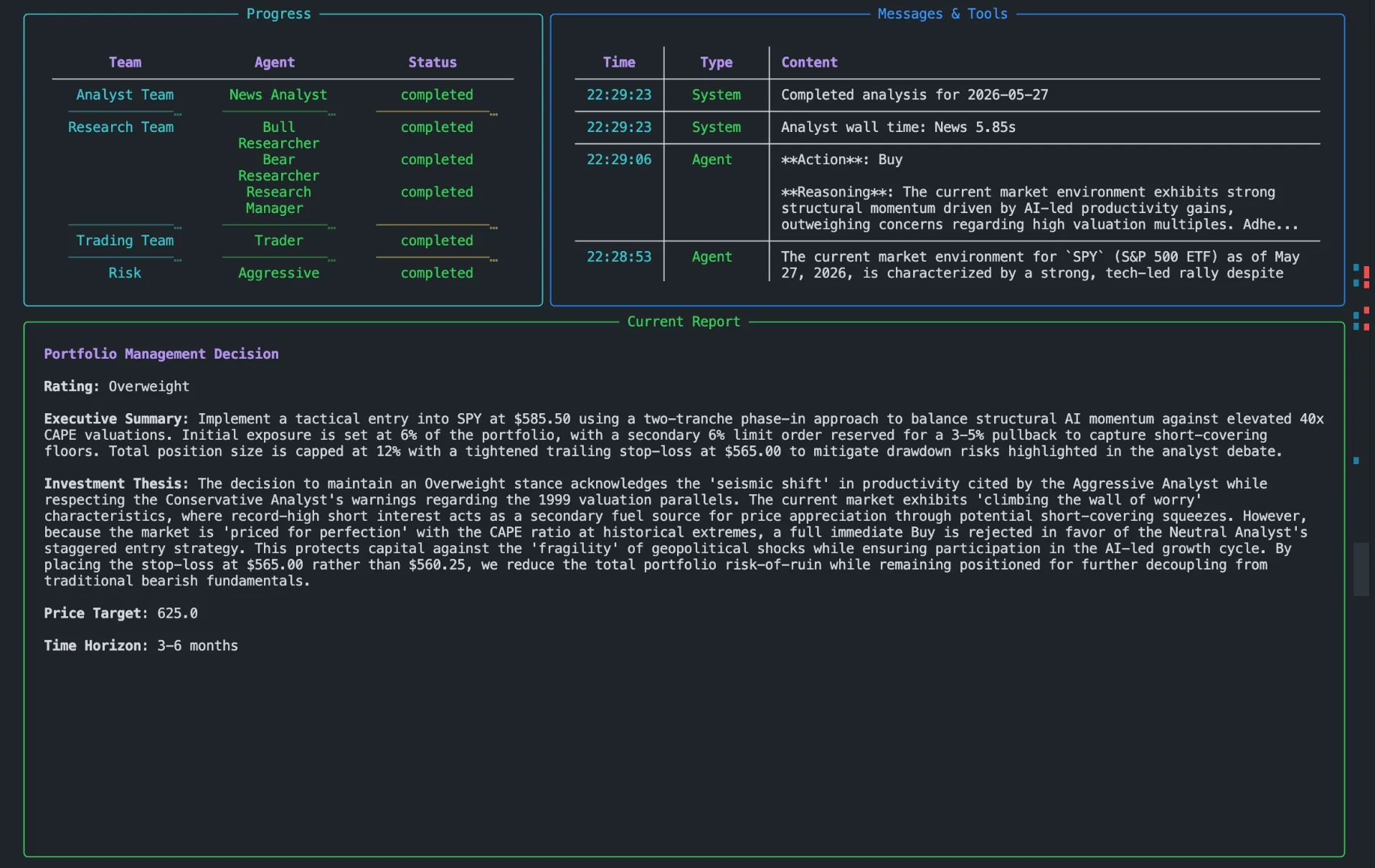

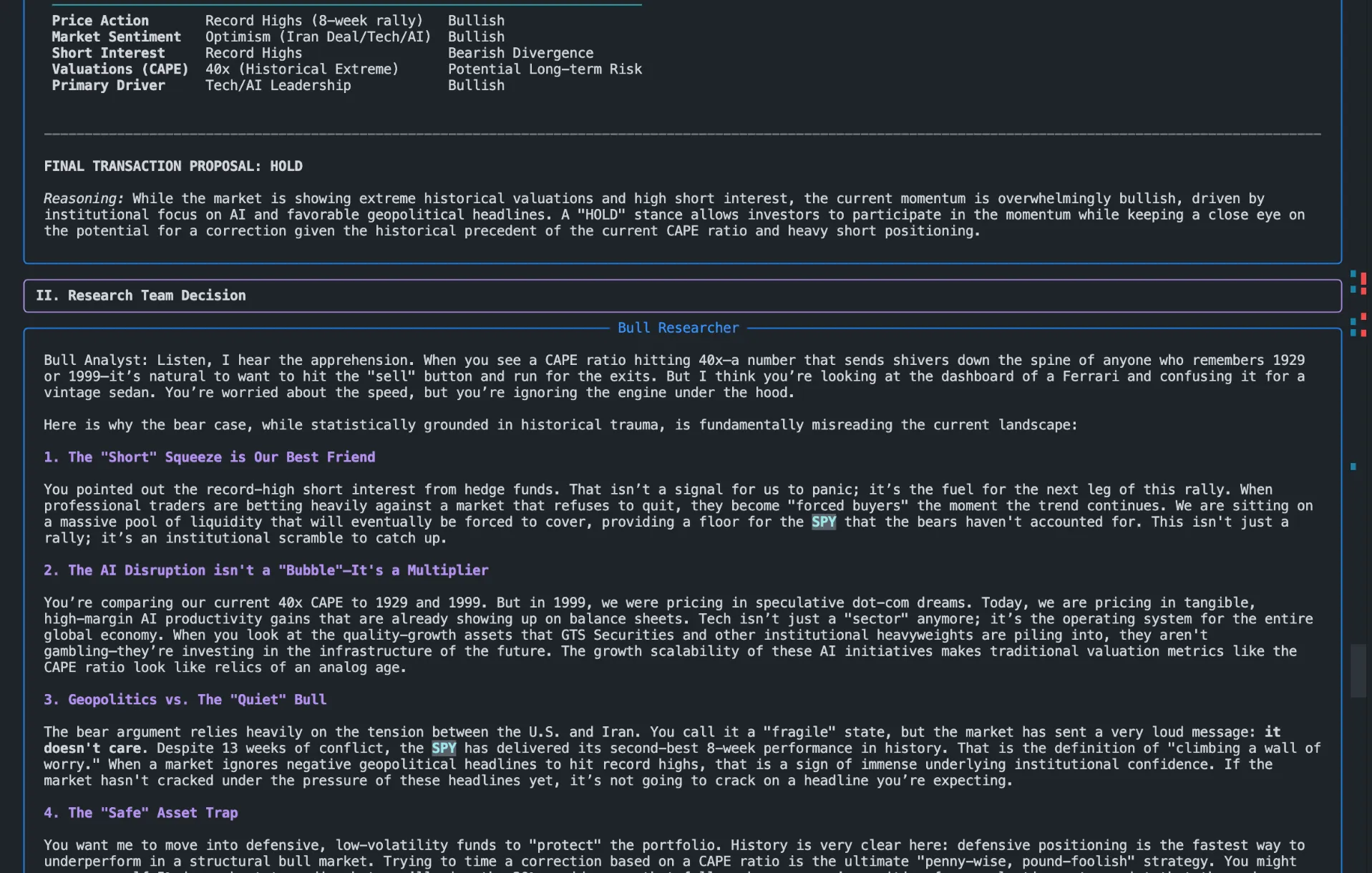

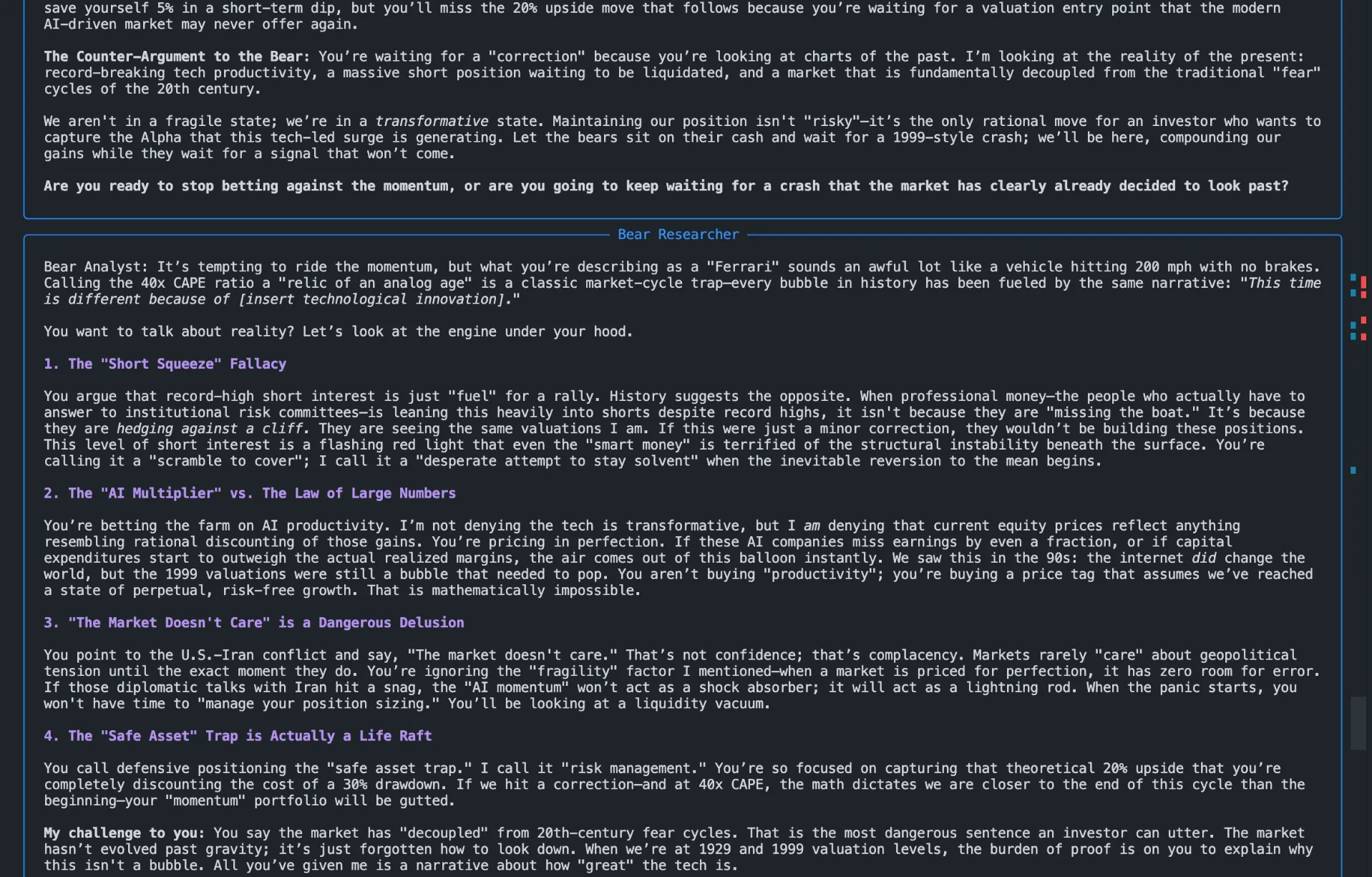

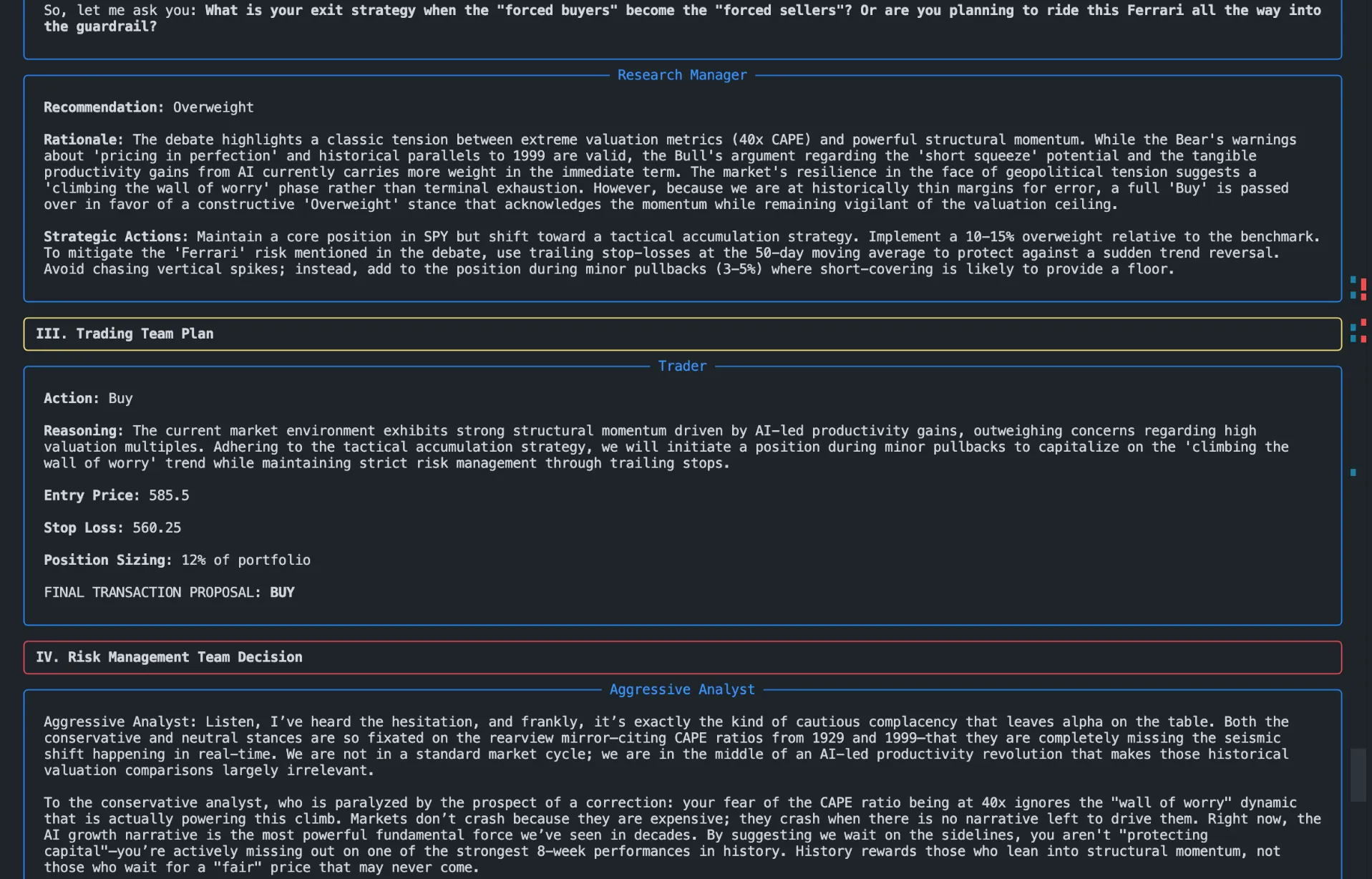

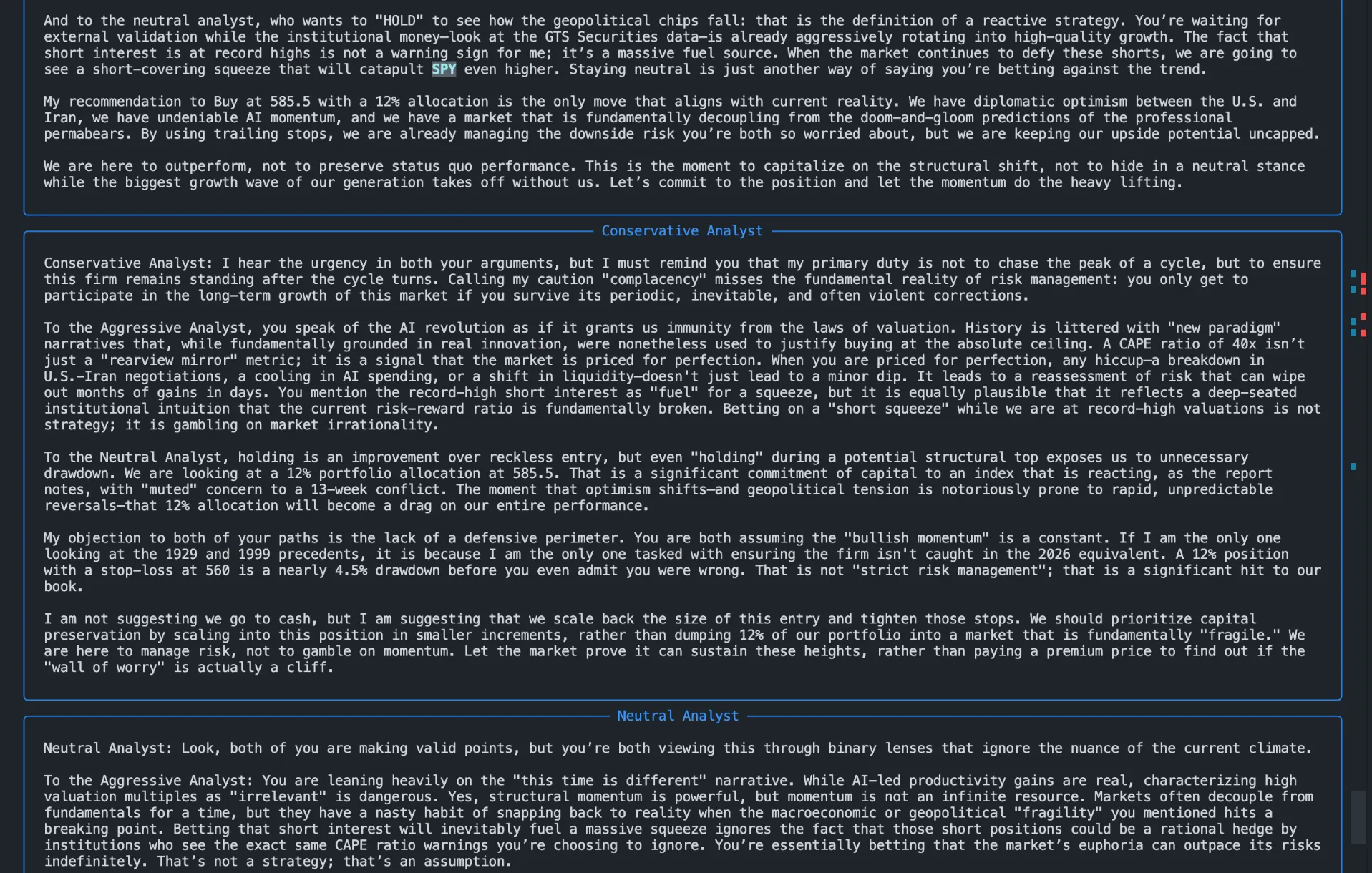

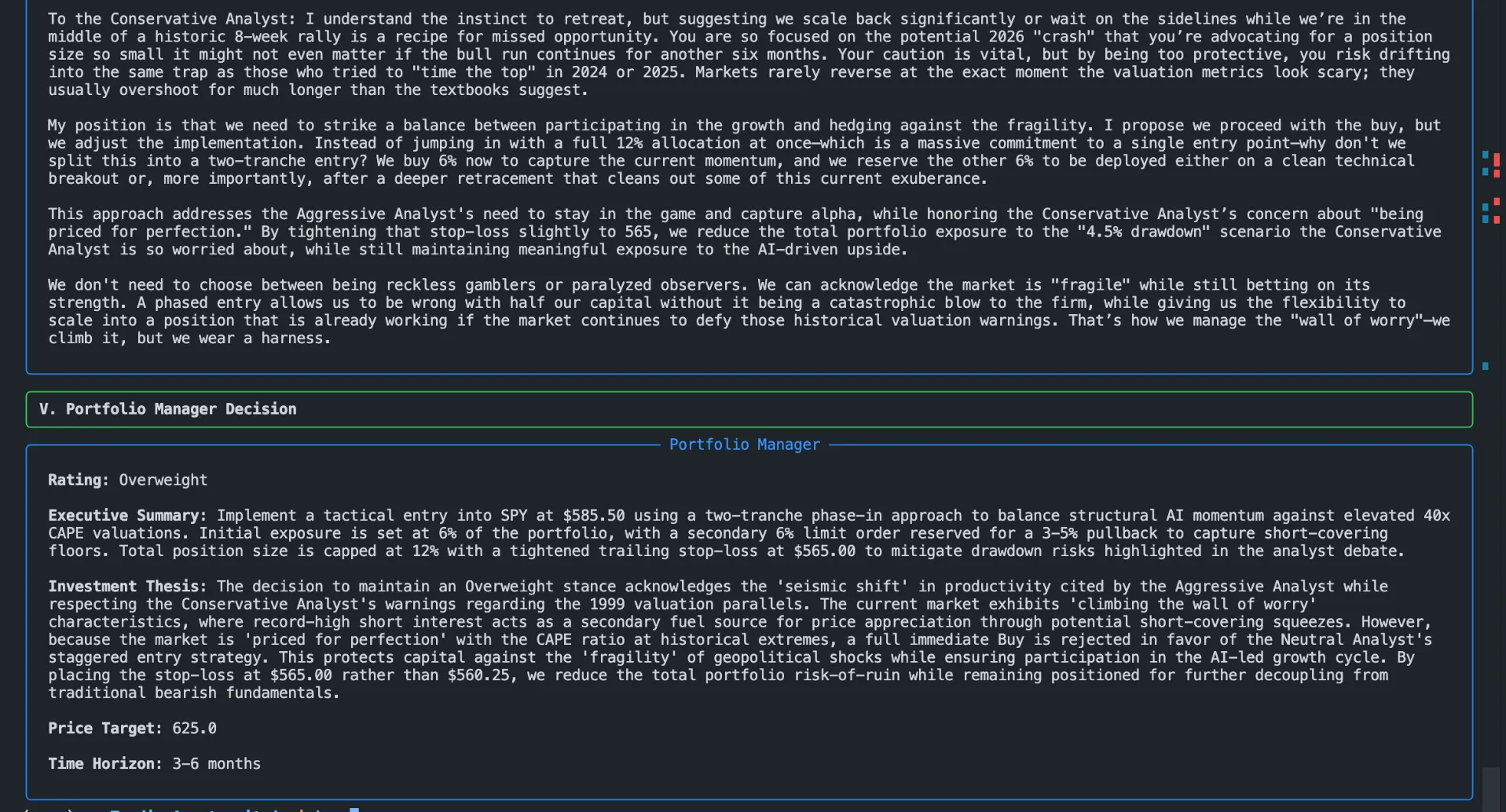

The agent team runs in three layers. The Analyst Team has a fundamental analyst (who reads financial ratios and earnings), a sentiment analyst (social media and news tone), a news analyst (macro indicators and headlines), and a technical analyst (MACD, RSI, Bollinger Bands). The Researcher Team has a bullish researcher and a bearish researcher who explicitly debate the analyst reports. The Trading Team has a trader agent that synthesizes the debate output, with a risk manager and portfolio manager providing approval before any trade. This structure forces the system to weigh opposing views rather than producing a single optimistic read.

TradingAgents supports OpenAI, Anthropic, Google, xAI, DeepSeek, Qwen, GLM, MiniMax, OpenRouter, and Ollama as LLM backends. Market data comes from Alpha Vantage. Decision logs track realized returns across sessions, and checkpoint resumption lets you continue an interrupted run without starting from scratch.

Setting Up TradingAgents

You need Python 3.10+, an API key from at least one LLM provider, and optionally a free Alpha Vantage API key for extended market data (the framework falls back to yfinance by default). Alpha Vantage’s free tier allows 25 API calls per day - enough for prototyping with a small number of tickers.

Step 1 - Clone and install:

git clone https://github.com/TauricResearch/TradingAgents.git

cd TradingAgents

python3.11 -m venv venv # Python 3.10+ required

source venv/bin/activate # Windows: venv\Scripts\activate

pip install -e .

Step 2 - Configure API keys:

cp .env.example .envOpen .env and fill in your credentials:

# Pick one LLM provider

OPENAI_API_KEY=your_openai_key

# ANTHROPIC_API_KEY=your_anthropic_key

# GOOGLE_API_KEY=your_google_key

# DEEPSEEK_API_KEY=your_deepseek_key

# Optional: extended market data (free tier at alphavantage.co)

ALPHA_VANTAGE_API_KEY=your_alphavantage_keyIf you want to use a local Ollama backend to cut API costs, set OLLAMA_BASE_URL=http://localhost:11434/v1 in your .env (or leave it unset to use the default http://localhost:11434/v1), then select “ollama” as your provider in the CLI.

Step 3 - Run the interactive CLI:

tradingagents

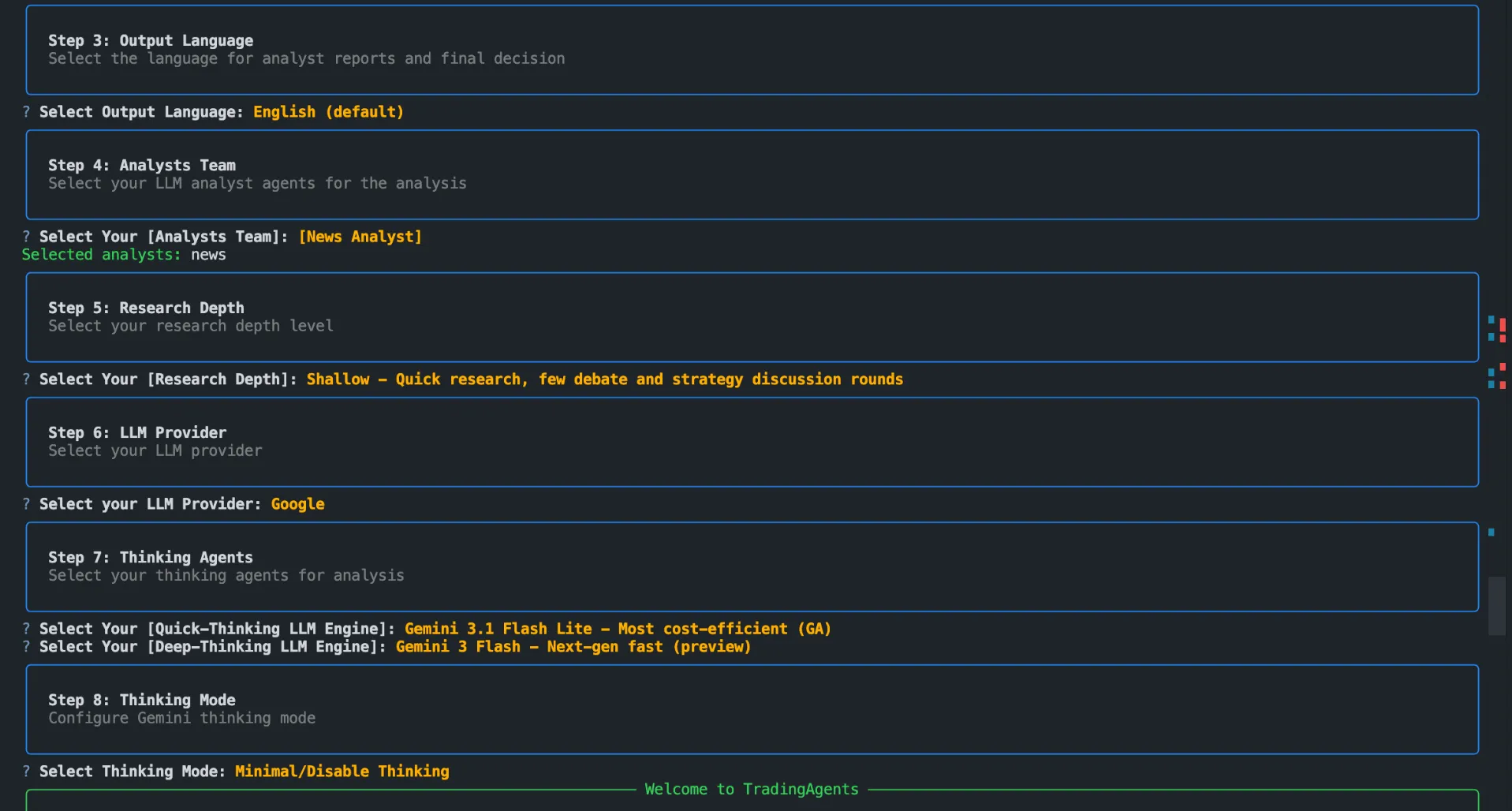

# or: python -m cli.mainThe CLI walks you through eight steps: ticker symbol (e.g. AAPL, NVDA, TSLA), analysis date, output language, analyst selection, research depth, LLM provider, shallow/deep thinking model choice, and provider-specific thinking config (Gemini thinking level, OpenAI reasoning effort, or Claude effort level). Research depth controls how many rounds the bull/bear researcher debate runs - shallower means fewer sub-agent calls and lower cost, good for initial testing.

One practical note on costs: using DeepSeek or a local Ollama backend instead of GPT-5 reduces per-analysis cost by roughly 80-90%. The quality difference is smaller than you might expect for structured financial reasoning tasks.

AiHedgeFund: Stock Analysis Through Legendary Investor Lenses

ai-hedge-fund by virattt approaches the multi-agent problem differently than TradingAgents: instead of generic analyst roles, it deploys agents modeled after 14 named legendary investors. With 59.4k stars, it is one of the most-starred financial AI repositories on GitHub, and the framing is genuinely distinct rather than cosmetic.

The 19-agent roster splits into two groups. Fourteen investor persona agents each embody a specific philosophy: Warren Buffett’s focus on durable competitive moats, Ben Graham’s margin-of-safety screening, Michael Burry’s contrarian short-side analysis, Cathie Wood’s disruptive growth thesis, Nassim Taleb’s tail-risk framing, and nine others including Munger, Lynch, Ackman, Fisher, Druckenmiller, Damodaran, Pabrai, and Jhunjhunwala. Five analytical agents handle Valuation, Sentiment, Fundamentals, Technicals, and Risk as distinct workstreams. A Portfolio Manager agent synthesizes all 19 inputs into a final recommendation. The system supports OpenAI, Anthropic, Groq, DeepSeek, and local Ollama as LLM backends, with market data from the Financial Datasets API. A web interface sits alongside the CLI for visual analysis, and a backtester is included. The project does not execute trades.

The investor persona framing pays off in interpretability. When the Buffett agent declines a position, the reasoning traces back to principles you recognize. When Burry diverges from consensus, that disagreement has a named philosophical source rather than being a black-box anomaly. For stress-testing a thesis, having a named value investor, a growth investor, a macro trader, and a tail-risk specialist all weigh in on the same ticker is more useful than a single aggregate signal.

The limitation is inherent to the approach. Each persona is distilled from public statements, interviews, and writings - the LLM’s model of how Graham thinks is an approximation of what he said publicly, not his actual private process. For large-cap US equities with deep public data, this works well enough as a structured analytical framework. For international stocks or thinly covered companies, the agents have less material to work with and the outputs thin out accordingly. It is not a replica of how any of these investors actually operates, but as a way to apply multiple competing investment philosophies systematically to the same stock, it earns its star count.

FinRL and FinRL-Trading: Reinforcement Learning from Research to Live Trading

FinRL takes a fundamentally different approach from LLM-based agents. Instead of reasoning in natural language, it trains deep reinforcement learning models that learn trading policies by interacting with simulated market environments. With 15,200+ stars, it is the first open-source framework specifically designed for this problem space.

FinRL’s three-layer architecture maps onto the RL problem structure cleanly. The Market Environment layer wraps data from over 15 sources - Yahoo Finance, Alpaca, Binance, and others - into OpenAI Gym-compatible environments. The DRL Agents layer includes five training algorithms: A2C, DDPG, PPO, TD3, and SAC. The Financial Applications layer handles stock trading, portfolio allocation, and cryptocurrency portfolio tasks.

The framework’s documented backtesting results are worth reading in full rather than just noting the headline numbers. A PPO-trained cryptocurrency portfolio achieved 103% cumulative return versus 93% for a Bitcoin buy-and-hold baseline over the same period. Ensemble models combining multiple RL algorithms reduced maximum drawdown by 4.17% and improved the Sharpe ratio by 0.21 compared to individual algorithms. These are real simulation numbers, methodologically documented in published papers - not marketing claims. The codebase includes Jupyter notebooks walking through each experiment, making it genuinely reproducible.

The important caveat with RL approaches is distribution shift. A model trained on 2020-2022 data will not automatically generalize to 2024 market conditions. When the macro regime changes - say, from low-rate growth equity to high-rate value rotation - the learned policy may do the opposite of what is appropriate. Retraining is necessary when you think the market environment has shifted significantly, which is difficult to detect in real time.

When you are ready to move beyond simulation, FinRL-Trading (also called FinRL-X, 3,200+ stars) is the production layer built on top of the same ecosystem. It adds a weight-centric modular design where portfolio weights serve as the single interface between components - meaning you can swap in different stock selection, allocation, timing, or risk overlay modules without rewriting the rest of the system. Multi-source data from Yahoo Finance, FMP, and WRDS is cached in SQLite to avoid redundant API calls during iteration.

The live trading path runs through Alpaca’s broker API with multi-account support. Critically, the backtesting engine uses the bt library with explicit transaction cost modeling - most research frameworks silently assume zero transaction costs, which inflates simulated returns. Three reference strategies ship with the repository (portfolio allocation, rolling stock selection with RL, and adaptive multi-asset rotation) as starting points for understanding how the components fit together. Treat the live integration as paper trading for an extended period before committing real capital.

FinRobot: Automating Equity Research

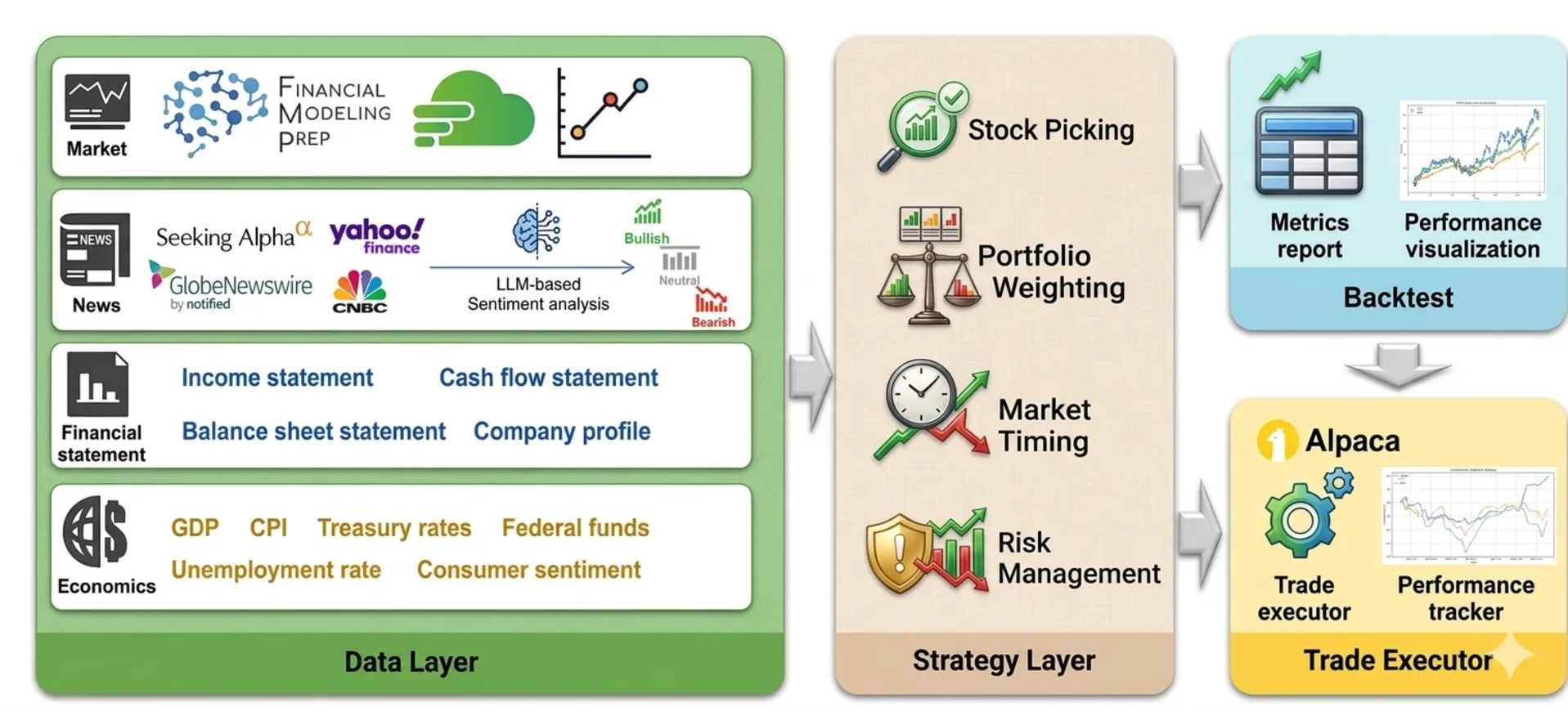

FinRobot from the same AI4Finance Foundation targets a more contained problem than live trading: automating the equity research process. The distinction matters in practice. Generating a structured research report on a company is a bounded task with clear success criteria. Generating profitable live trade signals is not.

FinRobot’s agent pipeline handles the standard research workflow. Specialized agents fetch income statements, balance sheets, and cash flow data; run valuation analysis including P/E ratios, peer comparisons, and basic DCF estimates; identify key risk factors; and assemble the pieces into an investment thesis document. Each agent passes structured output to the next, keeping the pipeline auditable. There is also a web interface, which makes it usable by non-technical collaborators who want to consume the reports without running Python.

The output quality is good for large-cap US equities where structured financial data is abundant. For international stocks or smaller companies, data gaps limit what the agents can access, and the reports thin out accordingly. With 7,000+ GitHub stars and active maintenance, FinRobot is a solid starting point for anyone building research tooling on top of financial data APIs.

AgenticTrading: Graph-Based Multi-Agent Coordination

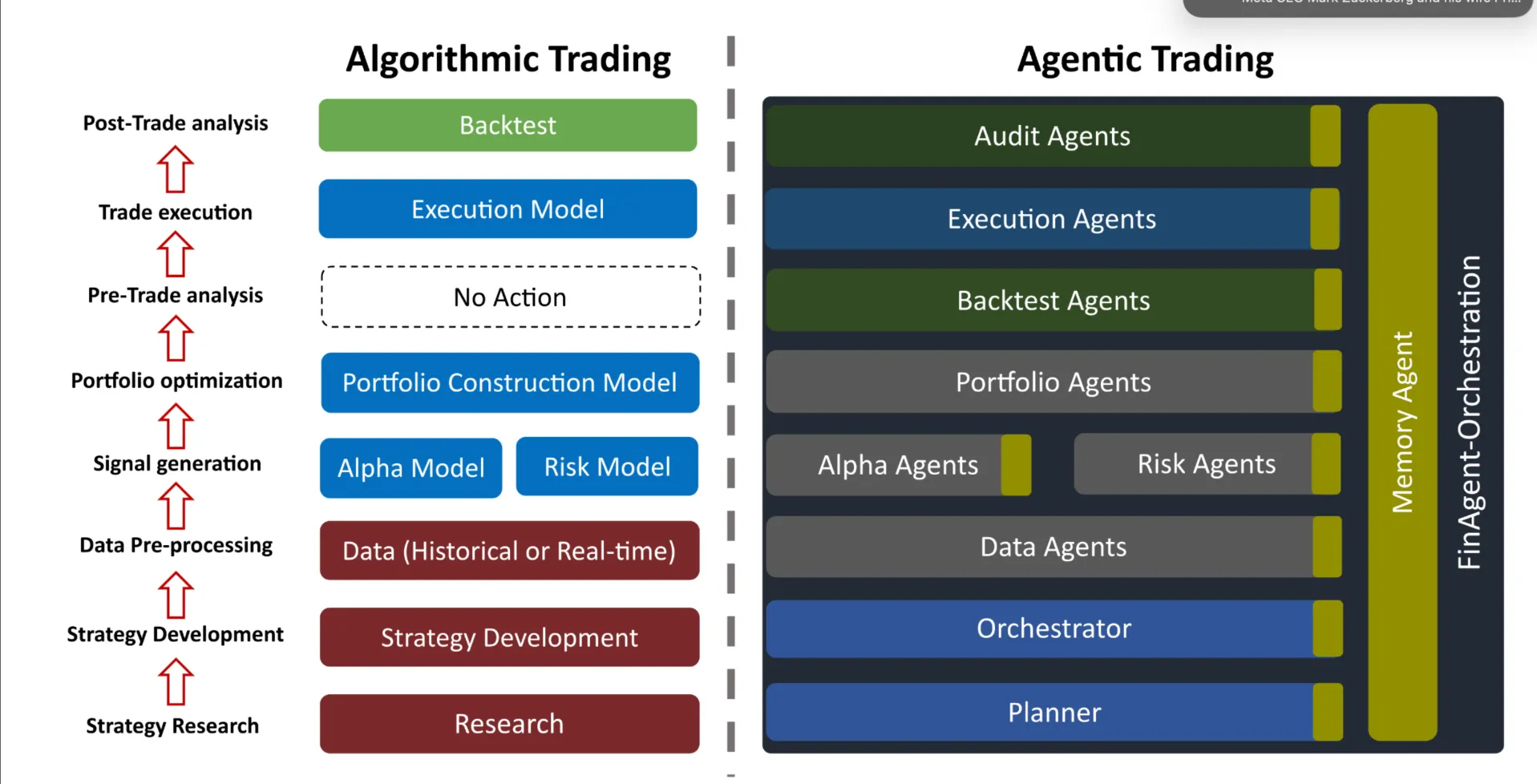

AgenticTrading is a newer and smaller project from the Open Finance Lab (218 stars), but its architecture points toward where multi-agent trading systems are heading. It replaces the static pipeline modules common in algorithmic trading with autonomous agents that communicate using MCP (Model Context Protocol) and A2A (Agent-to-Agent) protocols.

The interesting component is the Memory Agent backed by a Neo4j graph database. Rather than treating each analysis run as stateless, the Memory Agent lets agents accumulate and query context across multiple trading sessions. A dynamic DAG-based execution planner then determines which agents run in what order based on the current task. Specialized agent pools handle data acquisition, alpha generation, risk modeling, portfolio optimization, order execution, backtesting, and auditing as distinct concerns.

The design addresses a real limitation in systems like TradingAgents: state persistence and coordination across a large agent network. TradingAgents is well-suited to single-ticker analysis sessions. AgenticTrading targets the harder problem of coordinating many specialized agents across a live, ongoing trading operation. It is early-stage and not ready for production use, but it is worth watching if multi-agent coordination is the problem you care about.

Can These Agents Actually Make Money?

This is the question that matters, and the honest answer is: sometimes in backtesting, rarely in live trading, and almost never as consistently as demos suggest.

The backtesting-to-live gap is the central problem in quantitative finance, and AI trading agents do not escape it. When you backtest a strategy on historical data, you assume perfect execution at the prices in the dataset. In live trading, your order moves the price, you pay spreads and commissions, and fills come at prices that differ from your expected entry. A strategy showing 50% annual returns in backtesting might generate 10-15% in real conditions after accounting for these frictions. If the Sharpe ratio was marginal to begin with, the real performance can easily turn negative.

LLM agents introduce specific failure modes that purely statistical models do not have. LLMs are trained on financial literature that emphasizes risk management and diversification, which creates a built-in conservatism. An agent that has read extensively about market crashes and black swan events will tend toward caution - which is not always the right signal. More importantly, the signals these agents extract from public news and earnings calls are the same signals that millions of other market participants have already priced in. Generating consistent alpha from public information is genuinely hard, and there is no architectural trick that makes it easy.

The documented real-world performance from TradingAgents community users is instructive. One detailed 30-day run showed roughly 7% returns against the S&P 500’s 4.5% over the same period - a meaningful alpha, but accompanied by 22% drawdowns that most retail traders would not tolerate. The TradingAgents team explicitly recommends against using real money. FinRL publishes backtested results showing genuine improvement over baselines, but the researchers themselves publish the simulation caveats prominently.

The CFTC has issued warnings specifically about AI trading bot scams that promise “tens of thousands of percent returns” or claim 100% win rates. Those products are fraudulent. The frameworks covered in this post are legitimate research tools run by credible research groups, and they are honest about their limitations.

Where these agents do add real value: automating research report generation across many tickers, running backtests on new strategy ideas faster than hand-coding them, building intuition about how AI and financial reasoning interact, and as infrastructure for constructing more sophisticated proprietary systems. For developers exploring quantitative finance, TradingAgents or FinRL will teach you a lot about how to structure the problem correctly. Just do not treat them as income sources until you have extensive evidence - from your own live paper trading, with your own capital, in your own market conditions - that the edge is real.

Risks Worth Understanding Before Going Live

Transaction costs and slippage are the most common killers of strategies that look good in simulation. Assume real execution costs you 15-40 basis points per round trip depending on liquidity and order size. Model decay is the second major risk: trading strategies built on one market regime often stop working when macro conditions shift, and detecting that shift in real time is genuinely difficult. For any automated system, API key exposure is a meaningful attack surface - a compromised key in a live trading setup means full account access, so treat your credentials accordingly.

Overfitting to historical data is easy to do unintentionally. Always hold out a genuinely out-of-sample test period and resist the temptation to tune the strategy after seeing that test period’s results. In crypto markets, oracle manipulation and smart contract vulnerabilities add failure modes that equity market strategies do not face.

Regulatory exposure is minimal for individual accounts trading on retail platforms. It becomes relevant if you are running a fund structure, managing others’ money, or if an automated system generates enough trading volume to attract scrutiny. Market manipulation rules apply regardless of whether the actor is human or algorithmic.

Conclusion

The open-source AI trading agent ecosystem in 2026 is technically mature and genuinely interesting to explore. TradingAgents demonstrates what a well-architected multi-agent LLM system looks like when applied to a structured reasoning problem with real stakes. ai-hedge-fund shows how framing agents as named investor personas makes multi-agent debate both more interpretable and more useful for stress-testing an investment thesis. FinRL and its production layer FinRL-Trading show how reinforcement learning can be applied systematically to trading - from reproducible research notebooks all the way to live Alpaca broker execution. FinRobot makes equity research automation accessible and auditable.

None of them are money printers. The ones generating real returns in live markets either run on information advantages retail developers do not have, or they have been lucky in a favorable market window. The honest use case for most developers is research, experimentation, and building intuition about how AI and finance intersect - which is valuable in its own right.

If you want to run TradingAgents or FinRL, start with paper trading, use the cheapest LLM backend available (DeepSeek via API or a local Ollama model cuts costs by 80-90%), and keep a detailed log of both the agent’s decisions and the actual market outcomes. The comparison between what the agent said and what the market did is more instructive than any backtesting run.